Macroeconomic Theory

Keynesian vs. Classical

Attendance

Agenda

1

Two Theoretical Perspectives

2

The Classical - Supply Side

3

The Keynesian - Demand Side

4

Review and to Do

Two Perspectives

Supply vs Demand

macroeconomic theory has two major components: theories that explore the supply side and those that analyze the demand side.

Supply side theory explores the economic factors that determine the economy’s potential to produce output.

Demand side focuses on whether this output can be sold (which may in turn change decisions to produce).

Supply Side

What limits the ability to produce?

Supply of labor?

Supply of natural resources?

Supply of financing?

Technology?

Demand Side

Does demand limit output before supply side limits bind (potential output)?

Insufficient spending can come from the main categories:

- Consumption, Investment, Government Spending, Exports

Insufficient spending can lead to declines in actual output and thus underutilized resources (i.e. unemployment)

A Mix

Quite clearly both supply and demand are required for actual production and employment

Different theories and analyses will emphasize different aspects of these ideas

Very often the supply vs. demand split is at the core of fundamental policy disagreements

Central Questions

When does one side or the other determine the actual level of activity?

How do supply and demand forces interact to affect macro outcomes?

Policy recommendations?

Demand side policies: tax cuts, stimulus checks, gov’t infrastructure spending, social safety net, lower interest rates/easier financing

Supply side policies: tax cuts, deregulation, inflation targeting monetary policy

The Classical - Supply Side

Potential

Potential Output

\(Y^*\) - a level of GDP consistent with full utilization of resources (full employment)

Potential Growth

At potential output, the economy can only grow if one of the following are improved:

- Natural Resources

- e.x. de-regulation to increase oil access

- Labor

- e.x. immigration, work-incentives, population growth incentives

- Human capital

- e.x. education

- Physical capital

- e.x. machinery, equipment and structures investment

- Supply of finance

- e.x. incentives for saving

The role of saving

While physical capital is accumulated through the investment decisions of firms, according to some economic theories, investment is made possible by savings. When people save rather than consume, their actions potentially release resources to be used for investment.

Therefore, from the supply-side perspective higher saving enhances growth in the economy because it makes investment in physical capital possible—which leads to increased Y*.

e.x. The “corn” model of the economy

Preferences for thrift

- time-preference

- Are people willing to wait to enjoy the satisfaction that comes from consumption? If people are more patient, the economy saves more, and therefore releases more resources for capital accumulation.

- what determines time-preference?

- culture?

- interest rates?

- tax rates?

The decision to invest

Investment

\(I\) - the purchase of machinery, equipment, software, IP, etc… to aid production with the expectation of future return.

Firms compare expected return to direct and opportunity costs

- technology can increase expected return

- tax policy can increase expected return or lower costs

- interest rate policy can lower costs

Note that investment also has a demand-side effect

Technology

Productivity

A measure of output relative to a unit of input (i.e. labor hours, machine hours, etc…)

Technology can increase productivity of both labor and capital

Technology often “embedded” in a capital good

Some debate over whether technology is biased toward skilled vs. unskilled labor productivity

Tax policy

- we currently offer some tax credits for R&D

- some economists argue that lower “capital gains” tax rates would encourage innovation

Supply side sum-up

- Supply side could be thought of as “potential output”

- preferences

- resources

- technology

- But are there automatic mechanisms to move the economy toward potential?

- The argument that there are is sometimes called “Classical Theory”

The Keynesian - Demand Side

What determines employment - Classical

Classical theory argues that demand (spending) does not constrain output - potential output is the only constraint

Demand shock counter mechanisms:

- interest rates

- wages

- prices of goods and services

What determines employment - Keynesian

Keynes (1883-1946) developed and popularized the notion that demand constrains output and employment

In this view, declines in demand are not countered by automatic mechanisms, and in fact may be made worse

Gov’t policy is required to regulate the level (but not necessarily type) of output and employment

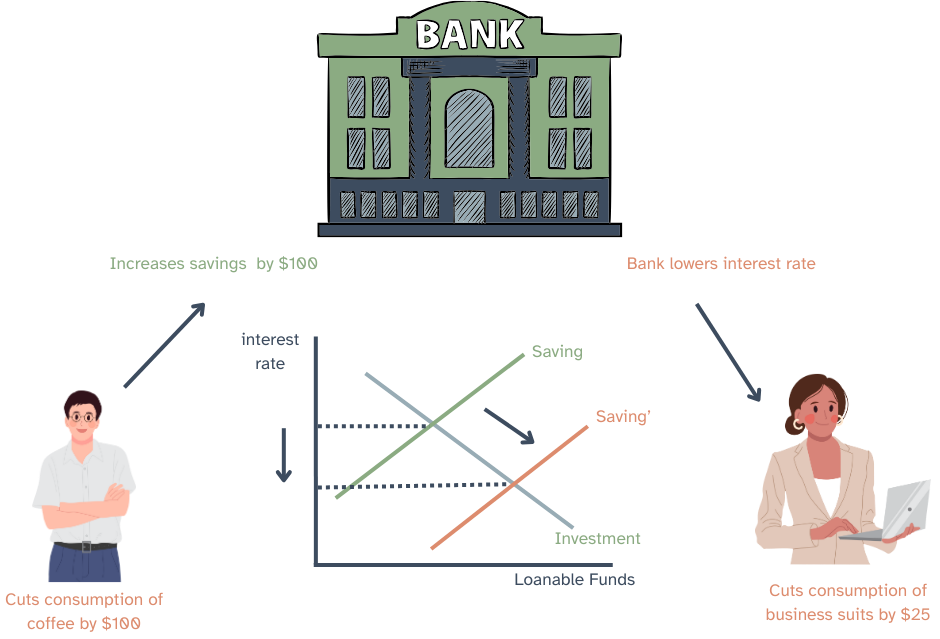

Loanable Funds Framework

Loanable Funds Framework

If I save money does it disappear?

The interest rate keeps falling until the supply and demand for loans again balances

- demand has shifted from consumer goods to investment goods

- Total demand remains equal to potential output (just like our corn economy)

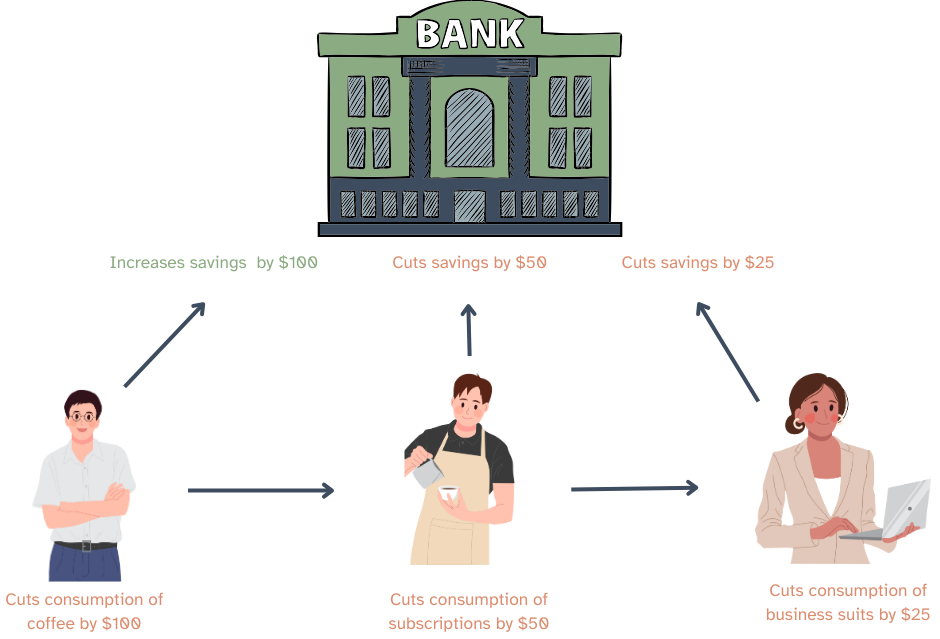

The Paradox of Thrift

The Paradox of Thrift

If I save money does it dissappear?

The decline in spending destroys income for other people

- they must cut their spending and likely their saving

By the time we sum up all the ripple effects of my decision, we find that actual savings in the bank have not increased at all, and consumption/income is lower!

The Paradox of Thrift

Paradox of Thrift

Individual attempts to save may increase that particular individual’s saving, but total saving in the economy does not increase.

- Since an increase in desired saving by some people does not increase the total saving in the economy, the supply of loanable funds never increases.

- there is no downward pressure on interest rates

In other words, when I save… the money does disappear from a macro perspective

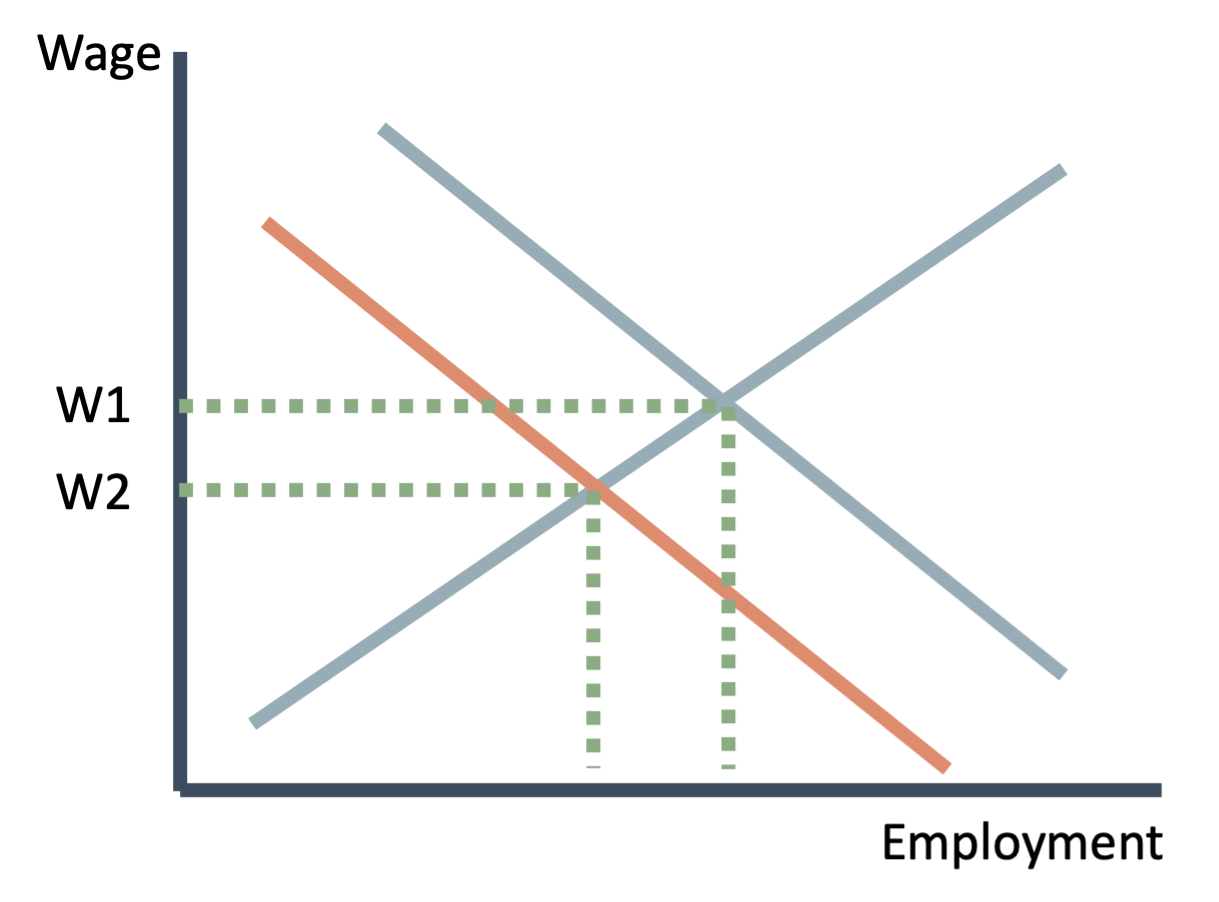

Wage and Price Adjustments

The Market for Labor

If demand falls, firms sell less, and fire workers… won’t wages decline?

falling wages should encourage employers to hire more workers

if wages fall, firms’ production costs will decline and perhaps this will lower prices, incentivizing more demand

Sticky Wages and prices

This perspective is widely shared among macroeconomists. Indeed the most widespread interpretation of Keynesian macroeconomics is that the theory only applies when wages or prices are somehow “sticky.”

Wages may be fixed by contracts

Prices may be sticky because of “menu” costs or customer retention concerns

If “stickiness” is the concern - perhaps the adjustment is working it just takes too long? In this case there may still be an argument for policy in the short run

Further detail

We actually can’t rely on a simple market model:

If the problem is insufficient demand, then falling wages won’t seem to raise demand

Falling wages might lead to falling prices, but why would this increase demand?

Macroeconomic Channels of Falling Wages/Prices

- wealth effect

- households with existing savings may find these are worth more when prices fall

- money demand effect

- households may find they need less money for daily transactions and so will buy financial assets or otherwise “release” these funds into financial markets.

- this may lower interest rates

Modern practice

These effects are generally accepted by many economists, but there is some question about how strong they are as mentioned earlier.

It may take a while for the deflation and interest rate effects to take hold, so perhaps we can speed things along by directly lowering interest rates through Federal Reserve policy

This would have happened anyway, so we aren’t really messing too much with the market mechanism

Problems with the standard view

However this story ignores some of the destabilizing effects of deflation:

- People may have wealth stocks, true, but others have debt stocks!

- this will be more difficult to service in deflation

- In deflation money is redistributed from debtors to wealth holders

- wealth holders may have a lower tendency to consume

- Perhaps people expect prices to fall further and so delay spending today

The Kenyesian Perspective

In normal times there is unemployment because demand is the primary limit on production

In times of crisis this gets much more severe

There are no automatic market mechanisms that will fix insufficient demand

Government has a role in determining the level of employment/economic activity

Review and to do

Summing Up

If demand falls…

Classical*

- Increased savings drive down interest rates and thus increase investment spending

- Lower wages/prices increase the value of wealth

- Lower wages/prices reduce money demand and thus drive down interest rates

Keynesian

- Income is destroyed leading to lower consumption and saving is unchanged

- Lower wages/prices increase the burden of debt

- Lower wages/prices redistribute from high to low propensity to spend households

- Lower wages/prices lead to postponed consumption

*actually this more accurately a description of the “Neoclassical Synthesis”

To-Do

1

Read

The Paradox of Thrift - For Real”

2

Do

No Assignments