Macroeconomic Theory

Investment

Agenda

1

Investment

2

Readings

3

Review and To Do

Attendance

Investment

What determines investment spending?

- Focus for a minute on investment in structures, equipment, software and R&D by private businesses (business fixed investment)

Firms must consider:

- cost of the investment

- cost of obtaining funds

- opportunity cost of funds

- predictions of future prices and demand

And all of this occurs at different dates!

Expected income

Firms must not only predict the stream of future income

- this expectation is precarious

The stream of income must also be valued in the present

The cost of investment

Two key costs:

costs of equipment

costs of funds

there are costs whether the funds come from internal reserves or external sources

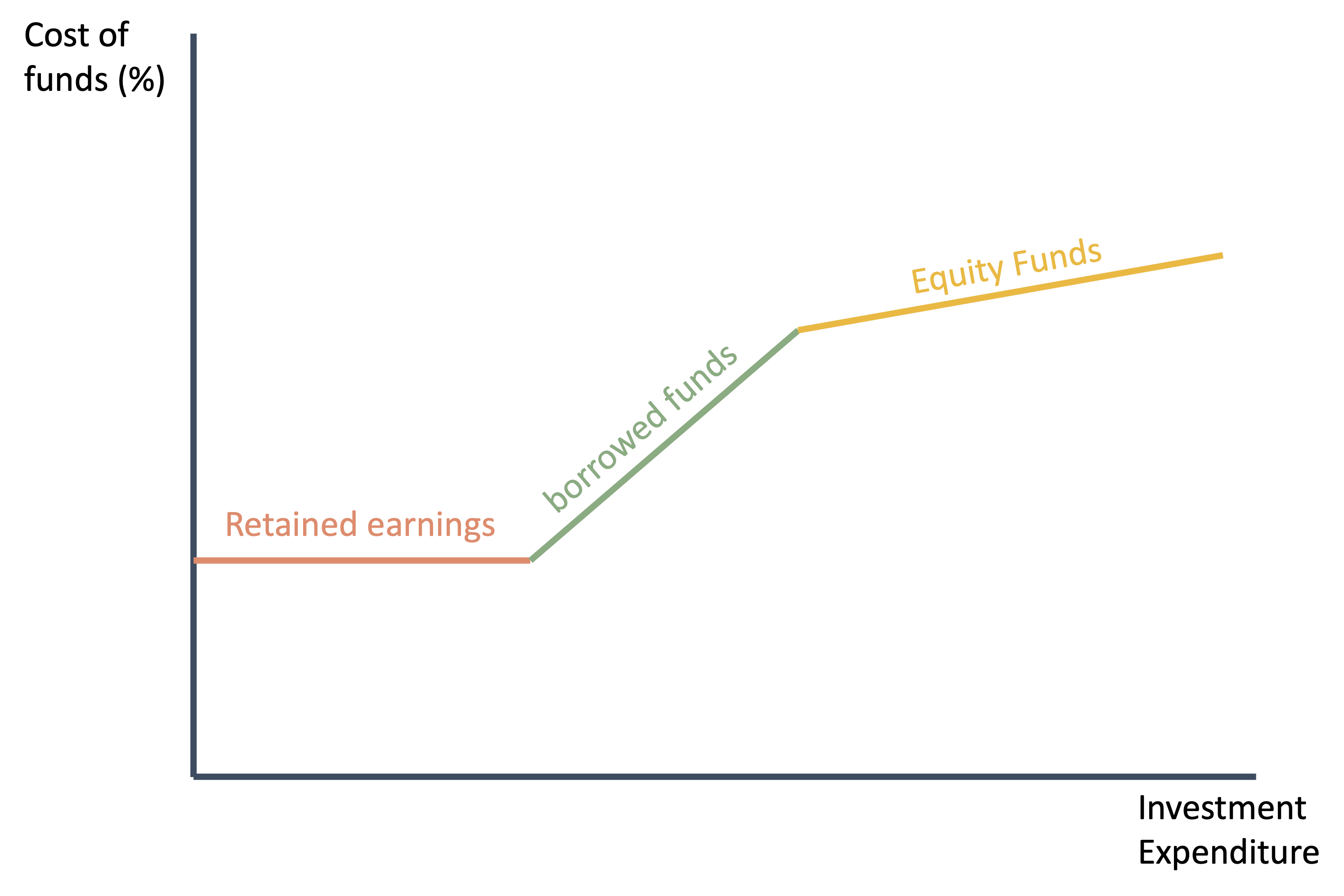

Sources of Funds

Retained earnings

Borrowing via bank loans

Borrowing via other debt instruments

Selling new equity shares

Borrowing sets up a stream of cash payments that legally need to be met

Discussion

Would you prefer $ 2 million when you retire in 45 years,

or $80,000 today that’s put into a bank account to

compound for the next 45 years? Explain in detail.

Compounding

The opportunity cost of an up-front investment is what would happen to that money if you put it somewhere to accumulate interest.

The amount that your money will grow into by a future date, as a result of earning interest, is called its future value.

\[ \text{Future value in t years} = \text{Present value} \times (1+i)^t\]

Discounting

The amount of money that you need to invest today in order to produce an equivalent benefit in the future is a present value.

Converting future values into their equivalent present values is called discounting.

Present value calculations

A simple version of a present value calculation would be a one time payment:

\[ \text{Present value} = \text{Future value in t years} \times \frac{1}{(1+i)^t} \]

Present value

- But investment calculation typically involves understanding the present value of a future stream of payments

\[ PV = \frac{Payment_{t+1}}{(1+i)} + \frac{Payment_{t+2}}{(1+i)^2} + \frac{Payment_{t+3}}{(1+i)^3} \]

- where \(i\) is the risk free rate of interest that you could get by loaning the money out

Present value

\[ PV = \frac{Payment_{t+1}}{(1+i)} + \frac{Payment_{t+2}}{(1+i)^2} + \frac{Payment_{t+3}}{(1+i)^3} \]

we would also want to modify this for the degree of risk/uncertainty

a firm can then compare the cost of funds to the expected present value of an investment good

The Interest Rate

It is common in macroeconomics courses to suggest that investment spending is inversely related to “the” rate of interest

As “the” rate of interest rises, both the cost of borrowing AND the opportunity cost of retained earnings rises

When compared with the present value of investment projects, this means that some projects will no longer have a present value that exceeds the cost of funds

The Interest Rate

You can use either interest rate in the compounding and discounting formulas:

If you’re evaluating the nominal value of your funds (how many bills you’ll have in a few years’ time), use the nominal interest rate.

If you’re evaluating the real value of your funds (changing purchasing power, after adjusting for inflation), use the real interest rate.

In practice, it is often hard to predict the relevant inflation rate over the life of an investment so real interest rates are very provisional.

How Sensitive is Investment to Interest Rates?

a common finding empirically however is that investment is not particularly interest elastic

Gormsen and Huber (2022) combed through “earnings calls” and flagged any mention of the hurdle rate or required return on new capital projects.

Hurdle rates are the minimum rate of return a business requires to undertake an investment project

They found that the hurdle rates were very high (15-20%) and did not seem to move with current interest rates

alternatively, housing investment (particularly by individuals) does seem to be fairly interest sensitive

Current income and investment

empirically, measures of current income and cash flow seem to exert a strong influence on business investment

this could be because cash flow is a source of funds, an indicator of credit quality, or serves as a predictor of future sales

- evidence for all three

this would imply a large multiplier than before since investment is responsive to current income

- it also suggests a link between short and long run economic performance

Financing Investment

Firms can finance investment through:

retained earnings

borrowing (issue bonds, or obtain bank loans)

equity (issue new shares)

Borrower and Lender’s Risk

If a firm uses retained earnings, it faces the opportunity cost of outstanding long-term debts (bonds) that it could have invested in.

If a firm borrows it will likely find that the more it borrows, the higher the rate it must pay

- lower cash flow ratio to fixed investment

- moral hazard

- note also the premium may change!

If a firm issues new equity, it may be expected to pay dividends (which have different tax treatment than interest payments), and as it issues more, outstanding shares are diluted.

Hierarchy of finance

Review and To Do

Review

Today we looked at some more complicated theories of consumption that argue consumers think about the future

- we found that while that is likely true, they are limited in their ability to bring future income into the present

We also got an introduction to the data and some elements of the investment decision

- we found that firms should respond to interest rates in theory, but don’t seem to in practice

- we also found that firms don’t consider all forms of finance equal

Readings

Do interest rates really drive the economy?

Two problems on the effectiveness of central bank interest rate policy - market rates don’t always follow Fed policy rates (we will discuss later ) - changes in interest rates don’t seem to have large effects on investment

Do interest rates really drive the economy?

relies on the Gormsen and Huber article we discussed earlier

In practice, business investment seems to depend much more on demand growth than on the cost of capital.

- can lead to vicious or virtuous spirals

all of this however suggests that the Fed may have a hard time controlling the economy

Interest rates just keep falling

When the C.B.O. projects how legislation will affect the economy, it assumes that when the government borrows more, higher deficits will cause interest rates to rise, crowding out investment by the private sector.

This has been orthodoxy and has been in intermediate macro courses forever, but it doesn’t seem to work in practice!

We will spend quite a bit of time discussing why it doesn’t work, but we might already have one version of an answer….

Crowding In and the Paradox of Thrift

If demand (output/income) drives investment more than interest rates, government spending might actually “crowd in” private investment!

Alternatively, when governments cut budget deficits - it seems to have a dampening effect on private investment.

Next time

Read:

Central Banking 101, Ch. 1-2

Money Creation in the Modern Economy

Do:

Homework 5