Macroeconomic Theory

Consumption cntd. and Investment

Attendance

Agenda

1

Finishing Consumption

2

Investment

3

Review and To Do

Attendance

Finishing Consumption

Forward looking

One critique of the classic Keynesian consumption function is that individual consumers are forward-looking decision makers.

The life-cycle theory emphasizes a family looking ahead over its entire lifetime.

The permanent-income theory distinguishes between permanent income, which a family expects to be long lasting, and transitory income, which a family expects to disappear shortly

Implications

Short run changes in income should not affect consumption decisions much

- This implies the consumption function is flatter than Keynesians thought

Stock of wealth matters

if a tax cut or increase in government spending is a short term even (like stimulus checks), it will be primarily saved because it does not increase lifetime income

Tests

Forward looking consumption definitely improved the predictive power of our consumption function

But there have also been empirical problems - consumption is still more responsive to temporary changes in income than forward-looking theories predict

Some refinements

Durable goods

Credit rationing/liquidity constraints

Credit rationing

Even non-durables seem to be more dependent on current income than we would think

The forward looking theories (particularly permanent income) assume that when someone has a bad year, they can maintaint their consumption

- this requires pre-existing wealth, or access to credit

Many households do not have stocks of wealth, and even more importantly, credit is often rationed

Credit Rationing

- Stiglitz and Weiss (1981)

Credit rationing occurs when people are unable to obtain funds at the relevant market rate of interest

Imperfect information may lead to demands for equity or collateral from borrowers

- Banks only lend to those who don’t need the money!

The “market for lemons” problem

Additionally, disadvantaged groups have been cut out of credit markets

Duesenberry

As you read, Duesnberry had an alternative explanation to Friedman and others

If the rich save at higher rates than poor, why doesn’t saving rise as everyone becomes richer?

Duesenberry’s explanation of the discrepancy is that poverty is relative. The poor save at lower rates, he argued, because the higher spending of others kindles aspirations they find difficult to meet.

Duesenberry argued that families look not only to the living standards of others, but also to their own past experience

In sum

We can say:

- Consumers try to smooth consumption

Wealth matters

Access to credit matters

Consumption is still pretty closely related to current income.

Investment

Investment in the National Accounts

Investment in structures by private businesses

- new non-residential and residential buildings, pipelines, railroad tracks, mines, etc…

Investment in equipment by private businesses

- equipment with service life > 1 year (computers, machinery, forklifts, etc…)

Investment in software, R&D, and entertainment originals

- this includes development and production of movies, TV, books, music

Investment in residential structures by owner occupants

Investment in structures and equipment and software by non-profit institutions

Inventories

changes in inventories are included in total investment in the NIPA accounts

Finished/ready for sale goods

work in process inventory

materials and supplies inventory

These are included in total income/gdp, but NOT in total demand

The Significance of Investment

Investment is one of the most volatile components of spending (along with consumer durables) so may be key to understanding business cycles

Investment also impacts long run productivity of the economy

- acquisition of capital goods which may enhance labor productivity and may also embody technology

What determines investment spending?

- Focus for a minute on investment in structures, equipment, software and R&D by private businesses (business fixed investment)

Firms must consider:

- cost of the investment

- cost of obtaining funds

- opportunity cost of funds

- predictions of future prices and demand

And all of this occurs at different dates!

Expected income

Firms must not only predict the stream of future income

- this expectation is precarious

The stream of income must also be valued in the present

The cost of investment

Two key costs:

costs of equipment

costs of funds

there are costs whether the funds come from internal reserves or external sources

Sources of Funds

Retained earnings

Borrowing via bank loans

Borrowing via other debt instruments

Selling new equity shares

Borrowing sets up a stream of cash payments that legally need to be met

Present value

Any investment calculation involves understanding the present value of a future stream of payments

$100 due in one year is worth less than $100 today… but how much less?

How much would you have to pay me in one year to get me to give up $100 today? $110? $120?

The answer is the rate of interest

Present value calculations

\[ PV = \frac{Payment_{t+1}}{(1+i)} + \frac{Payment_{t+2}}{(1+i)^2} + \frac{Payment_{t+3}}{(1+i)^3} \]

where \(i\) is the risk free rate of interest that you could get by loaning the money out

we would also want to modify this for the degree of risk/uncertainty

a firm can then compare the cost of funds to the expected present value of an investment good

The Interest Rate

It is common in macroeconomics courses to suggest that investment spending is inversely related to “the” rate of interest

As “the” rate of interest rises, both the cost of borrowing AND the opportunity cost of retained earnings rises

When compared with the present value of investment projects, this means that some projects will no longer have a present value that exceeds the cost of funds

How Sensitive is Investment to Interest Rates?

a common finding empirically however is that investment is not particularly interest elastic

Gormsen and Huber (2022) combed through “earnings calls” and flagged any mention of the hurdle rate or required return on new capital projects.

Hurdle rates are the minimum rate of return a business requires to undertake an investment project

They found that the hurdle rates were very high (15-20%) and did not seem to move with current interest rates

alternatively, housing investment (particularly by individuals) does seem to be fairly interest sensitive

Current income and investment

empirically, measures of current income and cash flow seem to exert a strong influence on business investment

this could be because cash flow is a source of funds, an indicator of credit quality, or serves as a predictor of future sales

- evidence for all three

this would imply a large multiplier than before since investment is responsive to current income

- it also suggests a link between short and long run economic performance

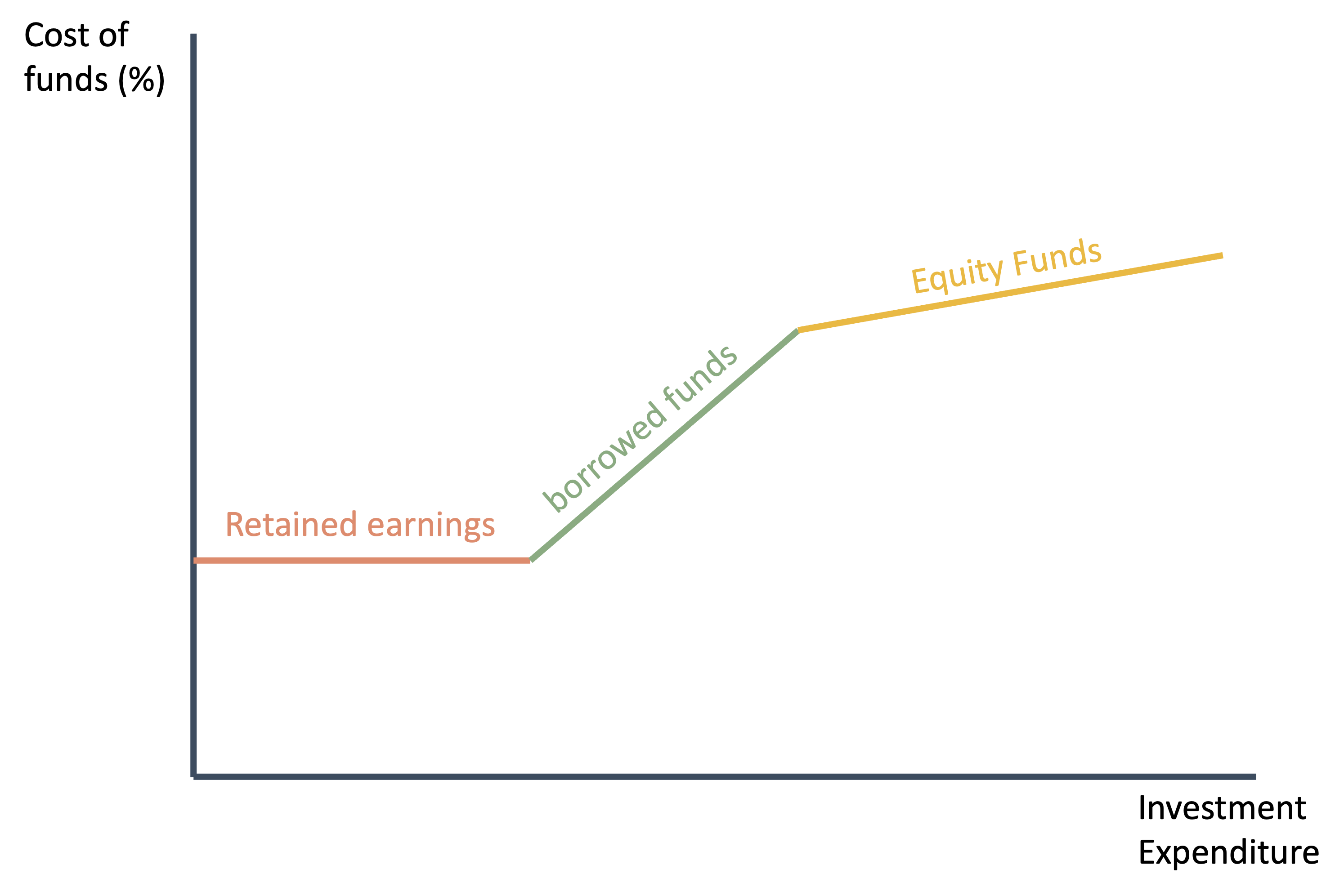

Financing Investment

Firms can finance investment through:

retained earnings

borrowing (issue bonds, or obtain bank loans)

equity (issue new shares)

Borrower and Lender’s Risk

If a firm uses retained earnings, it faces the opportunity cost of outstanding long-term debts (bonds) that it could have invested in.

If a firm borrows it will likely find that the more it borrows, the higher the rate it must pay

- lower cash flow ratio to fixed investment

- moral hazard

- note also the premium may change!

If a firm issues new equity, it may be expected to pay dividends (which have different tax treatment than interest payments), and as it issues more, outstanding shares are diluted.

Hierarchy of finance

Review and To Do

Review

Today we looked at some more complicated theories of consumption that argue consumers think about the future

- we found that while that is likely true, they are limited in their ability to bring future income into the present

We also got an introduction to the data and some elements of the investment decision

- we found that firms should respond to interest rates in theory, but don’t seem to in practice

- we also found that firms don’t consider all forms of finance equal

Next time

Read:

Do Interest Rates Really Drive the Economy? by J.W. Mason, The Slackwire

Crowding In and the Paradox of Thrift by Paul Krugman, NYT

Interest Rates Just Keep Falling. Economic Orthodoxy Is Falling With Them. by Neil Irwin, NYT

Do:

Homework 5